Driving Forces

The regulatory, economic, and strategic factors sustaining Japan's cybersecurity investment cycle

Japan's cybersecurity market is approaching ¥2 trillion ($13B+) and growing at double-digit rates. This isn't a cyclical trend — it's driven by structural forces that make sustained investment inevitable. For vendors evaluating Japan market entry, understanding these drivers is essential to timing and positioning.

Notably, analyst forecasts have consistently underestimated Japan's cybersecurity growth — IDC's 2022 projections for 2027 were surpassed ahead of schedule, prompting significant upward revisions.

Japan's cybersecurity market is not just large — it's structurally compelled to grow. Government mandates are creating compliance-driven demand floors. The identity and cloud security segments are growing fastest, reflecting Japan's accelerating digital transformation. For vendors with strong channel partner networks, the market dynamics are exceptionally favorable. The question is no longer whether to enter Japan, but how quickly you can build the right partnerships.

Sources: JNSA 2024 Survey Report (July 2025), IDC Japan Security Software Tracker (2025), ITR Market View: Cyber Security 2025, Japan Cabinet Office Economic Measures (Nov 2025)

Which pure-play cybersecurity vendors have the broadest channel partner coverage — based on documented partnerships across 128 Japan channel partners

Palo Alto Networks dominates with 24 Japan channel partners — the widest distribution of any pure-play cybersecurity vendor. This reflects both market maturity and aggressive channel investment.

Trend Micro (19) and Okta (18) round out the top three, followed by a cluster of vendors in the 15-16 range: Barracuda Networks, CrowdStrike, and Fortinet — all competing intensely for partner mindshare.

The long tail is telling: even well-funded vendors like Deep Instinct, Netskope, and Darktrace have fewer than 10 Japan partners, suggesting significant room for channel expansion.

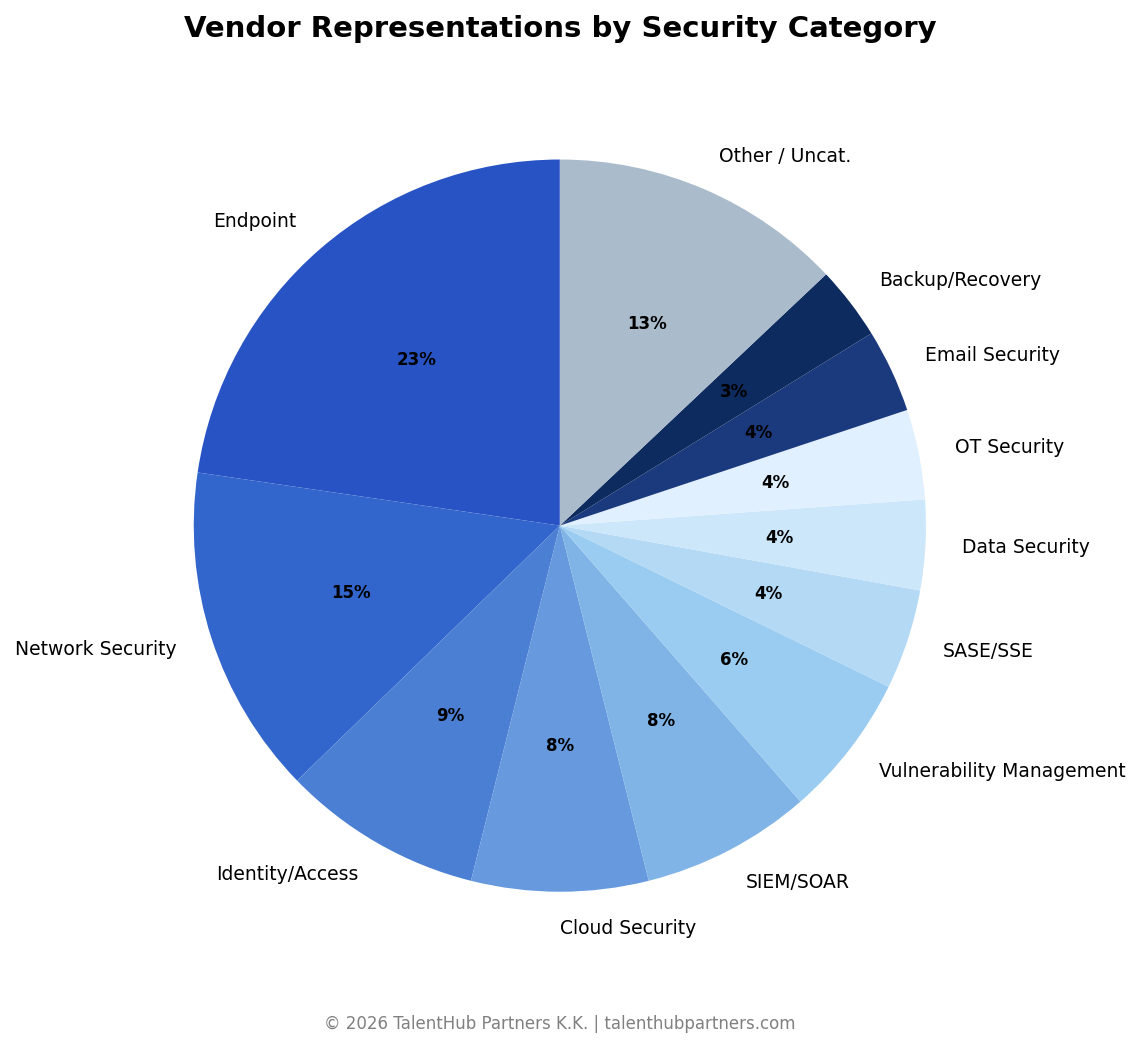

How 481 vendor representations break down across 11 cybersecurity categories

Category distribution | © 2026 TalentHub Partners K.K.

Endpoint security dominates at 23% of all vendor representations — reflecting both the maturity of the category and the sheer number of global vendors competing for Japan channel access. Network Security (15%) and Identity/Access (9%) round out the top three, together accounting for nearly half of all documented partnerships.

Notably, emerging categories like SASE/SSE (6%) and OT Security (4%) are growing fast. Several partners are actively adding vendors in these spaces, suggesting these categories will look very different by Q3 2026.

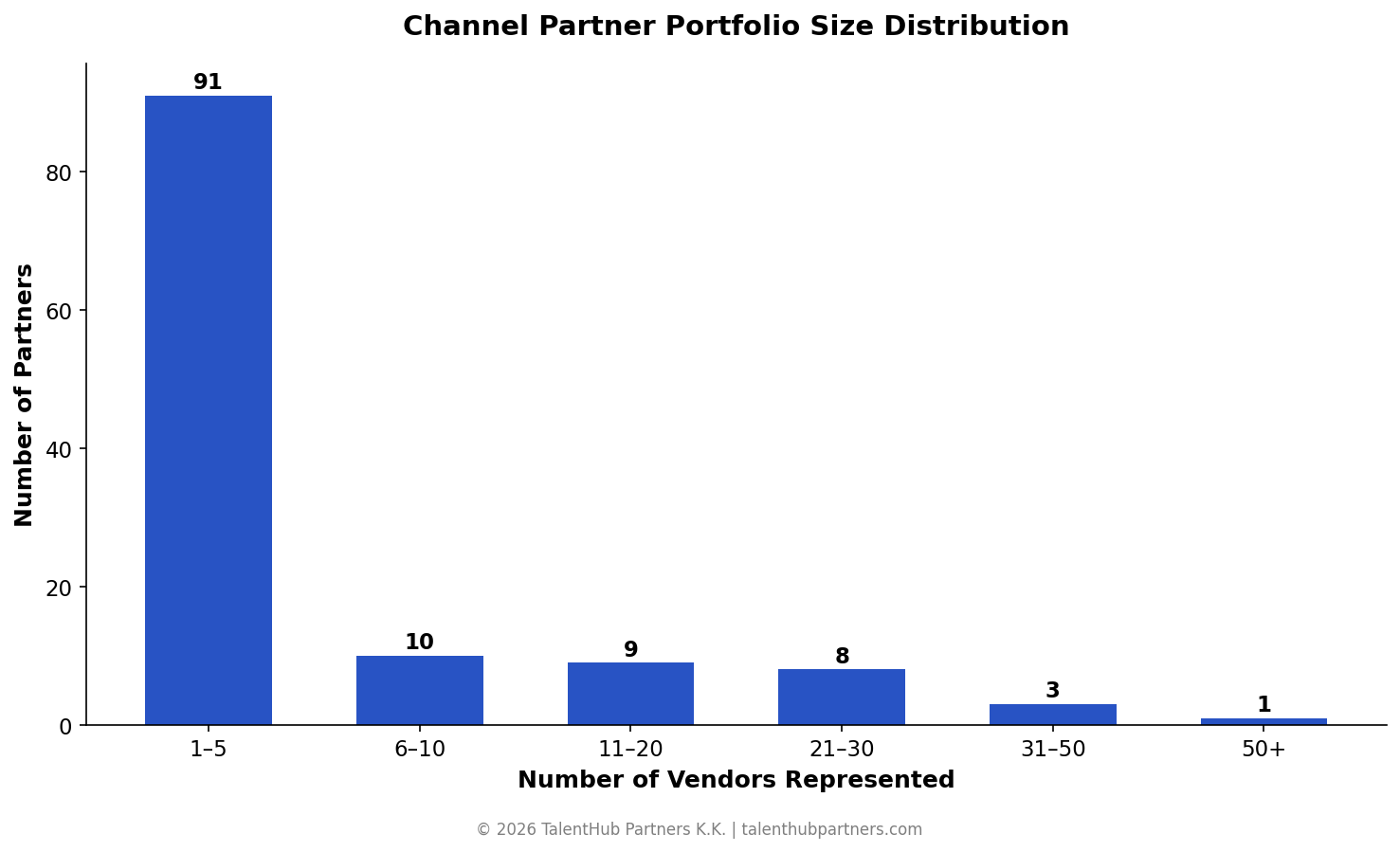

The concentration pattern — most partners carry few vendors, a handful dominate

Portfolio size distribution | © 2026 TalentHub Partners K.K.

The long tail is real. 91 of 128 partners (63%) carry five or fewer global cybersecurity vendors — meaning most Japan channel partners are specialists, not generalists. Only 12 partners carry more than 20 vendors, and just one (Hitachi Solutions at 44) has built a truly broad-spectrum cybersecurity practice.

For vendors evaluating Japan channel strategy, this concentration matters: partnering with a top-15 partner gives you instant access to a mature security practice, but competing for attention against 20+ other vendors in their portfolio. Partnering with a specialist means exclusivity — but a narrower reach.

Category Highlights

Endpoint security dominates with 154 vendor representations (23% of total), reflecting the mature installed base of EDR/XDR solutions across Japanese enterprises.

SASE/SSE is the fastest-growing category — 30 vendor representations today, but growing rapidly as Zscaler, Netskope, and Cato Networks aggressively expand their Japan channel partnerships.

The full report includes deep-dive analysis of each category, heatmap coverage matrices, whitespace identification for new market entrants, and M&A-driven consolidation patterns...

Where Japan's top 15 channel partners have documented coverage (●) and where potential opportunities may exist (○)

How to read this map

Each row represents one of Japan's top 15 channel partners. Each column represents a cybersecurity category. A filled cell (●) means we found documented evidence of that partner carrying at least one vendor in that category. An open cell (○) means no vendor relationship was found — a potential gap in their portfolio.

Open circles are not confirmed absences — partners may carry unlisted vendors or have capabilities through adjacent product lines. But directionally, they indicate where a partner's portfolio may be thin.

Why this matters for vendors

If you're a vendor looking to bring your solution to Japan, this map tells you which partners already have strength in your category — and which ones have gaps you could fill. A partner with a weak portfolio in your space is a partner looking for exactly what you offer.

For example, SASE/SSE and OT Security show the most open circles — meaning fewer partners carry vendors in these categories. That's either a market that hasn't matured yet, or an opportunity for vendors in those spaces to approach partners who need to round out their offerings.

📊 The full report includes a granular version of this heatmap — broken down by individual vendor names within each cell, showing exactly which vendors each partner carries in each category. Available in the downloadable PDF.

| Partner | Endpoint | Network Security | Identity/Access | Cloud Security | SASE/SSE | Data Security | SIEM/SOAR | Email Security | OT Security | Vuln. Mgmt | Backup/Recovery | Score |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Hitachi Solutions (44) | ● | ● | ● | ● | ● | ● | ● | ● | ● | ● | ● | 11/11 |

| TED (30) | ● | ● | ● | ● | ● | ● | ● | ○ | ● | ● | ● | 10/11 |

| SB C&S (26) | ● | ● | ● | ● | ● | ● | ● | ● | ● | ● | ● | 11/11 |

| SCSK (24) | ● | ● | ● | ● | ● | ● | ● | ● | ○ | ● | ○ | 9/11 |

| Hitachi Systems (23) | ● | ● | ● | ● | ○ | ● | ● | ● | ○ | ● | ● | 9/11 |

| Macnica (23) | ● | ● | ● | ● | ● | ● | ● | ● | ○ | ○ | ○ | 8/11 |

| LAC (21) | ● | ● | ● | ● | ● | ○ | ● | ○ | ○ | ● | ○ | 7/11 |

| Kanematsu (20) | ● | ● | ● | ● | ● | ● | ● | ○ | ● | ○ | ● | 9/11 |

| CTC (19) | ● | ● | ● | ● | ● | ● | ● | ○ | ○ | ● | ● | 9/11 |

| TechMatrix (19) | ● | ● | ● | ● | ○ | ○ | ● | ● | ○ | ● | ● | 8/11 |

| Cybernet Systems (17) | ● | ● | ● | ● | ● | ● | ○ | ● | ● | ● | ○ | 9/11 |

| NESIC (16) | ● | ● | ○ | ● | ● | ● | ● | ○ | ● | ● | ○ | 8/11 |

| SoftBank (14) | ● | ● | ● | ● | ● | ○ | ○ | ● | ● | ● | ○ | 8/11 |

| NetWorld (13) | ● | ● | ● | ○ | ○ | ○ | ○ | ● | ○ | ● | ● | 6/11 |

| NEC (12) | ● | ● | ● | ○ | ● | ○ | ● | ● | ● | ● | ● | 9/11 |

Based on documented vendor partnerships from public sources. Open circles indicate potential gaps — not confirmed absence. Partners may carry unlisted vendors or have capabilities through adjacent product lines. © 2026 TalentHub Partners K.K.

What's Happening Now

Recent events, launches, and partner activity from Q4 2025–Q1 2026 — showing where vendors are actively investing in Japan channel development.

Highlights

Flagship event with Security Days Fall presence across Tokyo, Osaka, Nagoya, and Fukuoka. JAPAC Distributor Excellence Award presented November 2025. Strongest event footprint of any vendor.

Regular webinars, hands-on FortiGate training, and a 9-session Security Operations Summit in December. Sustained investment in partner and customer enablement.

Announced first Japan distribution agreement. Presence at Security Days Fall Tokyo. Signals aggressive Japan market entry by the cloud security leader.

CTC signed first domestic distribution agreement with U.S. data security vendor Cyberhaven, followed by a Digital Workplace for AI event in February. A new entrant to watch.

TEDconnect2025 featured sessions from SentinelOne, Semperis, F5, Netskope, Rubrik, and Thales. Followed by a joint ransomware defence seminar (SentinelOne + Semperis + Rubrik) in March 2026. TED is emerging as a cybersecurity distribution powerhouse.

Next-gen MDR attack demonstration webinar. CrowdStrike continues to invest in technical enablement for its 16-partner Japan channel.

Annual flagship event. With the Splunk acquisition complete, Cisco's security portfolio pitch to Japan partners now spans network + SIEM + observability.

What This Tells Us

October is peak season. 12 of 33 events concentrated in October 2025 — aligned with Japan's fiscal H2 budget cycles and Security Days conferences.

Distributors are becoming event platforms. TED's multi-vendor showcases and CTC's new vendor launches show distributors moving beyond logistics into market-making.

New entrants are moving fast. Wiz, Cyberhaven, and Semperis all made Japan channel moves in this period — signalling that the market is still attracting new global vendors.

Event data sourced from vendor websites, partner announcements, prtimes.jp, and conference programmes. Coverage is representative, not exhaustive. © 2026 TalentHub Partners K.K.